I’ve been getting a lot of calls lately, from my clients as well as folks with other insurance companies.

“Why is my car/home insurance so high?”

It’s a fair question.

There are two reasons rates keep getting higher and it’s true for both home and auto insurance.

1) The number of claims is going up. (You can blame bad drivers and climate change for that)

2) Claims are getting more expensive. (Inflation, worker shortages and supply chain issues get the credit here)

To put it another way, insurance is a way of spreading out the pain. And there’s been a lot of pain to go around lately.

So, the question becomes, “How do I save money on my insurance?”

1) Get a local agent. Yes, I am an agent and yes, this one is a bit self-serving. But we’re specialists. Find a couple of specialists and ask them for quotes. Make them explain what coverages they’re recommending and why. Go with the one who can come up with the best combination of price and coverage.

You won’t get that from an 800 number or a website.

An agent can also help you decide whether decide whether anything else on this list makes sense for you.

2) Take a look at your deductibles and other “extras” like rental reimbursement.

This one comes with a really big caveat: Don’t lower your liability limits or how much you’re insuring your home for. Rates are going up because you’re more likely to need your insurance. Now is not the time to start skimping.

That said, you will be able to save money by raising your deductible. You’ll have to decide whether the lower premium is worth the higher risk.

If raising your car insurance deductible from $500 to $1,000 saves you $60 a year, keep the $500 deductible.

But if raising your home insurance deductible from $1,500 to $2,500 saves you $300 a year? That’s probably worth it.

And if there are two drivers and three vehicles, do you really need rental reimbursement on your auto insurance? Or would you be able to use the third vehicle?

3) Credit score. Yeah, sorry, that one affects your rate, too.

Underwriters say there’s a correlation between how well you keep track of your finances and how likely you are to have a claim.

So, if your life is more stable than it was when you first started your insurance, it may be worth asking your agent for the company to rerate you based on who you are now.

And if you’re asking around for quotes, make sure the agent checks whether it’s cheaper to put you or your spouse as the first named insured (That’s whose credit they’ll check).

BTW, it is considered a “soft hit” so getting an insurance quote doesn’t affect your credit score.

4) Discounts. This the one that all the ads like to talk about. And a local agent can help find discounts you didn’t know you qualified for.

A quick rundown of a few you may not know about:

- Bundling (Package several types of policies like home, auto, life, business, boats, etc., together and you usually get them cheaper than getting them each individually. I’ve even seen instances where the package was cheaper than the auto by itself)

- Homeowner (For auto insurance)

- Good student (As if you needed another reason to encourage the kid to get good grades)

- Pay plan (The cheapest ways to pay are usually pay all at once or with an automatic draft from a checking account)

- Where you work (Sometimes your occupation can get you a discount)

- ePolicy (Get your policy emailed to you instead of a hard copy)

- Early shopping (Yes, you can get a discount if you don’t need to start your insurance right away)

- Updated equipment (Have you updated your plumbing, HVAC or electrical systems? You may be able to reduce your home insurance premium)

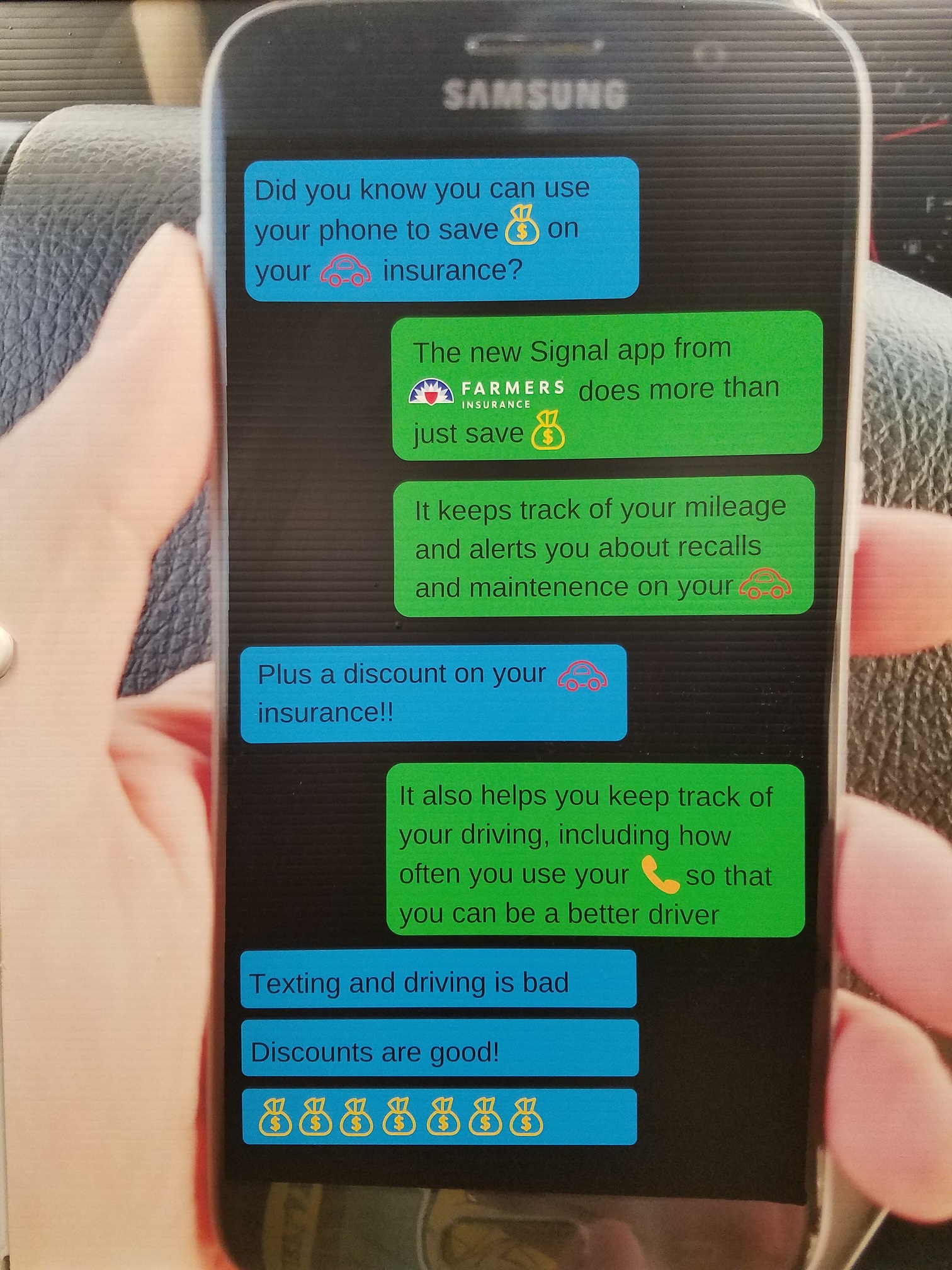

5) Auto trackers. Technically this one’s a discount, but these are worth talking about a little more.

Before I started selling insurance, I got a discount for plugging a little doohickey into my car that kept track of some of my driving habits. That was almost 15 years ago.

Now most companies have a phone app that monitor your speed, your mileage, and — probably most importantly — when you’re on your phone as you drive. (Remember when I said there are more crashes because of bad drivers? Drivers distracted by their cell phones is right at the top of the list of problems)

I was hesitant when Farmers rolled its out, but the app isn’t doing anything your phone doesn’t already do, it’s just sending the information to one more place.

These apps are a few years old now and I expect them to get more important as time goes on.

I had one client tell me she found an insurance company where she could “pay as you go.” The trick is not crossing the line between tracking and stalking.

Unfortunately, folks, there are no magic bullets, just a couple of suggestions until we get past the current craziness.