Unless you have some weird, cut-rate version of home insurance, all policies are going to cover the basics.

Fire, tornado, theft, falling space debris, you know, the usual stuff.

An attack by a giant, fire-breathing lizard?

Probably covered.

But there are four disasters that are not going to be covered unless you specifically add them.

1) Flood. That’s the one that’s on everyone’s mind right now, for stuff like this and this.

Flood insurance is handled by the National Flood Insurance Program and it’s a separate policy from your regular homeowners insurance.

If you live in a 100-year flood plain, your mortgage holder will require you to buy flood insurance (and they’ll notify you of the requirement before they give you a mortgage).

As side note, a “100-year flood plain” does not mean the area’s going to flood once a century. It’s shorthand for an area that has a 1 percent or greater chance of flooding in any given year. In other words, there’s a 26 percent chance of flooding during a 30-year mortgage.

I’ve seen places on a 50-year flood plain — which means there’s a 2 percent chance of flooding in any year — flood twice in five years.

But even folks who aren’t on a flood plain need insurance: According to the NFIP, 20 percent to 25 percent of all flood claims come from low-risk areas.

2) Sinkholes. What could be worse than the ground opening up to swallow everything you own? Finding out that most home insurance policies exclude “earth movement.”

That’s kind of a big deal for those of us here in Missouri. There’s a reason the Show Me State is also known as the Cave State. See, here’s one. And all the recent rain is making them even more threatening, like this one.

There aren’t many insurance companies that will help you here. I know of two and although Farmers isn’t one, Foremost (one of the companies we work with) is. If you’re worried about a sinkhole, you may be better off with the Missouri FAIR Plan’s standalone policy for sinkholes, similar to what the National Flood Insurance Program’s flood insurance.

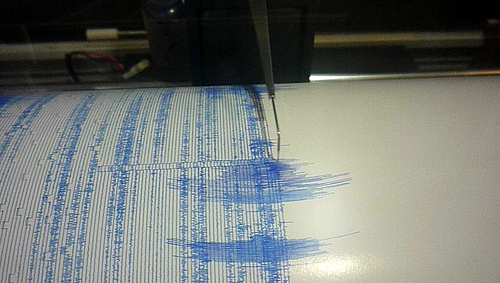

3) Earthquake. The “earth movement” exclusion falls into play here, too.

But there’s not much to worry about here, right?

A few small temblors around the Ozarks, mainly on the south side of the Missouri border, but nothing to be afraid of.

Except there’s that one thing you learned in school. Here’s how the state’s Department of Natural Resources puts it:

Most Missourians have heard of the more recent 1811-1812 flurry of quakes that were in the range of magnitude 7-8 and centered near New Madrid, Missouri. Because few people lived in Missouri in the early 1800s, impact to human life was minimal. The three major earthquakes in late 1811 and early 1812, however, did permanently change the course of the Mississippi River and created the Reelfoot Lake in the northwest corner of Tennessee.

Yeah, the largest earthquake in the country happened over on the east side of the state. Not a whole lot of people in Missouri two hundred years ago, so no biggie.

Any idea of what it would do now?

Out of the four big gaps in your home insurance coverage, earthquake is typically the easiest to fix. You just tell your agent you want to add an earthquake endorsement. It doesn’t add much to your premium — typically somewhere between $35 and $100 a year. However, the deductible is usually between 5 percent and 25 percent of your home’s value.

And in case you’re wondering, the earthquake endorsement only covers earthquakes, not sinkholes.

4. The death of a breadwinner.

This is the one that should be keeping you awake at night if you don’t have a policy in place to protect your family.

We like to think about our home being our biggest asset, but it’s not. Our biggest asset is our ability to earn money. If you’re not there to earn that money, what happens to the house? What happens to the people inside it?

Life insurance is not for you.

Life insurance is for the ones you leave behind.

It’s to make sure they can keep the house you’ve been working so hard to provide.

It’s to make sure they have food on the table and clothes on their backs.

It’s to make sure they can keep living the life you wanted for them.

All four of the disasters on this list are scary.

But No. 4 is the one that would have the longest impact on your family.

[…] how would have an agent been able to help him? Because his claims were both caused by flooding. Floods aren’t covered by home insurance. An agent could have told him that before it reached the claims stage so it didn’t count […]

LikeLike

[…] Earthquakes are one of four disasters that your home insurance doesn’t normally cover. […]

LikeLike